In November 2025, the European Commission announced the Sustainable Transport Investment Plan (STIP), a roadmap under the EU Clean Industrial Deal to mobilize funding for the decarbonization of the aviation and waterborne transport sectors.

The aviation sector plays a significant role in the EU economy, contributing over €110 billion to GDP and employing up to 281,000 people.[1][2] At the same time it is the second largest contributor to EU transport sectors GHG emissions (13.8%). The maritime transport sector contributes around € 61.8 billion to GDP and employs approximately 393,000 people, while being responsible for 12.7% of transport sector emissions.[3] Both sectors are considered hard-to-abate due to their almost 99% reliance on fossil fuels,[4] posing a significant lever to reduce transport sector emissions by 90% by mid-century to achieve the EU’s goal to become climate-neutral by 2050.[5] Their decarbonization will require a combination of measures, including efficiency improvements, the development and deployment of alternative propulsion technologies, and in some cases modal shifts.

Within this broader transition, the STIP focuses primarily on accelerating investment in sustainable aviation and maritime fuels (SAF and SMF) as a central lever for near-to medium-term emissions reductions.

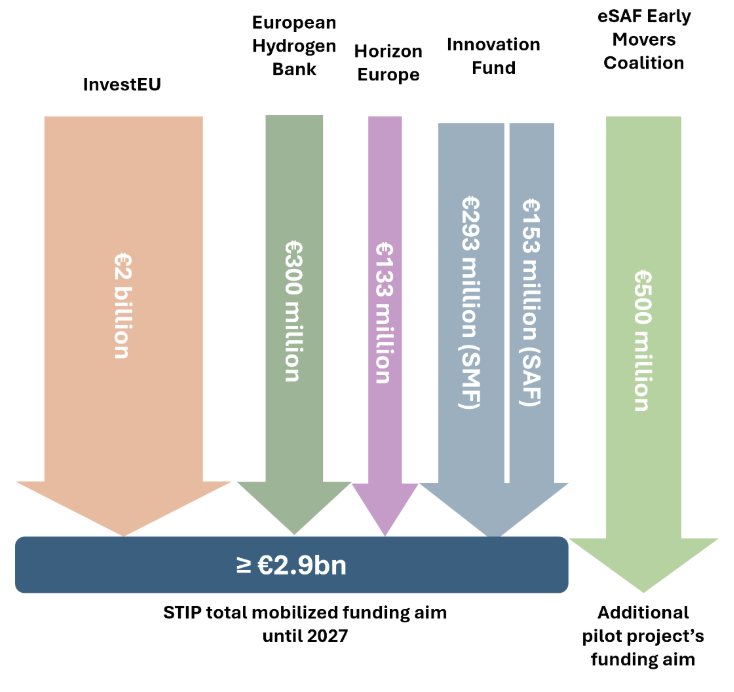

While the STIP specifies that at least €2.9 billion of initial funding will be mobilized by 2027 through various EU instruments (see Figure 1), meeting the ReFuelEU Aviation and FuelEU Maritime fuel targets will require approximately €100 billion by 2035. In parallel, the European Commission will also introduce additional mechanisms through the STIP, aiming to provide revenue certainty and de-risk investments, while reducing administrative burdens to free up resources for growth.[6]

Figure 1. Contribution by funding instrument to anticipated mobilized funding under the STIP.[6]

UNEP FI and the European Banking Federation (EBF) recently convened EU policy makers, banks and industry representatives to identify market and financing-related challenges and opportunities following the introduction of the STIP. While several issues are sector-specific, a clear message emerged: the European Union still requires stronger incentives, long-term demand signals, targeted de-risking mechanisms to unlock finance and stable long-term policies to make the transition of aviation and shipping a reality.

Policymakers and representatives of the banking, shipping and aviation industries discussed the necessity of long-term policy certainty and stable demand signals; blended financing to bridge cost gaps; scaling up guarantees, de-risking mechanisms and further public financial support; use of ecosystem approaches and demand-side tools; and ensuring that the EU regulation, including financial regulation, is conducive to the transition in the aviation and maritime sectors and their financing. This article highlights takeaways from their discussions.

Provide long-term policy certainty and stable demand signals

Predictable, long-term regulatory frameworks are needed to enhance the business case and underpin investment decisions. For aviation, this includes maintaining stable SAF mandates, ensuring a more linear increase in demand and providing multiannual or ex-ante allocation of allowances to support long-term offtake agreements and investment cases for SAF. For maritime, the EU Emissions Trading System (ETS) is seen as the primary driver, but participants highlighted the need for a broader “basket” of policy tools and more consistent implementation of the Renewable Energy Directive (RED) III. Participants noted that without stable demand signals, projects struggle to reach final investment decisions and most remain commercially unviable and therefore unbankable.

Combine financing instruments to bridge the cost gap

No single policy instrument will enhance the business case and bankability on its own. A combination of mechanisms is needed, with emphasis on double-sided auctions, along with complementary instruments such as carbon contracts for difference (CCfDs), ETS-based funding streams and other tools, to bridge the price gap between low-emission fuels and conventional alternatives. In a double-sided auction, a central intermediary contracts with both suppliers and offtakers, reducing credit risk for the supplier and protecting buyers from future price volatility. If there is a gap between supply and demand bids, the intermediary can use public or industry-based funding, such as revenues from penalties or other existing funding streams, to cover the remaining price difference and help stabilize market expectations. Making clean fuels cost-competitive remains central to scaling deployment.

Scale up guarantees, de-risking and public financial support

Public financing alone will not meet the scale of investment needed; stronger public risk-sharing is required to crowd in private capital. It is essential to provide effective public financial support and de-risking tools to move projects through early stages, cover technology and market risks, and support clean fuel production in Europe, as well as infrastructure and retrofitting of vessels. Export credit support, guarantees, and grants to bring projects to an investable level and larger guarantee facilities were all cited as necessary. More public first-loss risk and stronger guarantees are needed to unlock financing for first-of-a-kind projects and emerging fuel value chains.

Use ecosystem approaches and demand-side tools

Given the complexity of both sectors, ecosystem approaches that bring together producers, offtakers, infrastructure providers, local communities and financiers were identified as critical. Clusters, green shipping corridors,[7] and shared infrastructure can aggregate demand, reduce risk, and support scaling.

Ensure that the EU regulation is conducive to the sector’s transition and its financing

Ensuring that EU regulation across sectors, including financial regulation, is conducive to the sectors’ transition and its financing was a recurring theme. Tensions can arise between financing needs for transition projects and risk-related prudential requirements; however, prudential requirements remain fundamental to a well-functioning financial system and should not differ from one sector to another. When associated with bankable business models, closer interactions between industrial policy, financial regulation and supervisory expectations can help enhance the competitiveness of EU aviation and shipping industries.

As discussions on the implementation of the Sustainable Transport Investment Plan and other initiatives within the Clean Industrial Deal continue, the workshop highlighted a shared message from banks, industry and policymakers: moving from policy ambition to bankable projects will require coordinated action, stronger incentives, targeted de-risking and long-term regulatory clarity.

UNEP FI and EBF will continue to support dialogue between financial institutions, industry and policymakers as the Clean Industrial Deal, STIP and related initiatives are further developed, helping to move from roadmap to deployment in Europe’s industrial transition.

[1] European Commission, Mobility and Transport. “Air – Internal Market”. 18 July 2025. https://transport.ec.europa.eu/transport-modes/air/internal-market_en

[2] European Union. “European climate law-aligned transition pathways . Sectoral fiche, Transport Air freight & passenger ». November 2025. https://op.europa.eu/en/publication-detail/-/publication/50f79539-bebb-11f0-a612-01aa75ed71a1

[3] Official numbers only available for maritime transport (excluding inland waterways): European Commission. “The EU Blue economy report 2025, Maritime transport”. 2025. https://op.europa.eu/webpub/mare/eu-blue-economy-report-2025/blue-economic-sectors/maritime-transport.html

[4] European Environment Agency. “Sustainability of Europe’s mobility systems – Energy” 10 October 2024. https://www.eea.europa.eu/en/analysis/publications/sustainability-of-europes-mobility-systems/energy

[5] Transport & Environment. “State of European Transport 2025”. 2025. https://www.transportenvironment.org/state-of-european-transport/state-of-transport-2025

[6] European Commission. “Commission unveils the Sustainable Transport Investment Plan: a strategic approach to boost renewable and low-carbon fuels for aviation and waterborne transport”. 5 November 2025. https://transport.ec.europa.eu/news-events/news/commission-unveils-sustainable-transport-investment-plan-strategic-approach-boost-renewable-and-low-2025-11-05_en

[7] Green shipping corridors are routes where vessels operate using low-emission propulsion, such as alternative fuels or electricity. They serve to assess the feasibility of deploying sustainable shipping means, including the entire marine ecosystem with actors like fuel producers, ports, vessel owners and cargo owners (Green Corridors)