Financial health and inclusion are central to economic resilience, enabling households and small businesses to manage shocks, invest, and participate in growth. Across Asia Pacific, the challenge is no longer only expanding access to financial services, but ensuring those services improve real financial outcomes, including improved financial resilience and financial health.

KEY TAKEAWAYS

- Financial inclusion in Asia Pacific has advanced significantly and is delivering measurable results in

expanding access - Access alone is not sufficient, as lasting financial stability depends on customer’s financial

resilience and overall financial health - Housing affordability and Small and Medium Enterprises (SMEs) financing remain key challenges

- Banks play a central role in translating access into real economic resilience

- The Principles for Responsible Banking (PRB) provides a practical implementation approach for

banks to fulfil that role

Asia Pacific’s Next Frontier of Responsible Banking

Progress has been substantial. Asia Pacific stands out among developing regions for high account ownership and digital financial adoption. As financial services become more widely accessible, customers in Asia Pacific are better positioned to absorb and recover from economic, health, or environmental shocks, making resilience the natural next frontier beyond inclusion. However, access does not automatically translate into resilience. While the share of adults able to rely on savings in an emergency increased by 6% between 2021 and 2024, many households and businesses remain financially vulnerable.[1]

This gap between access and outcomes highlights the importance of financial health. UNEP FI defines financial health as the ability to manage finances, absorb shocks, and plan ahead, expanding the focus from financial access to financial resilience.[2]

- 83% of adults in East Asia and the Pacific have a financial account, up from 69% a decade ago

- +20% of global mobile money accounts are in East Asia & Pacific

- 56% of adults in East Asia & Pacific can access emergency funds

Source: World Bank

There is a clear business case for prioritizing financial health. By focusing on the financial well-being of consumers, financial institutions not only build trust and loyalty but also open the door to increased spending and investment by consumers. This can lead to new opportunities for cross-selling and a reduction in credit risks. Financially healthy customers are the bedrock of a stable and flourishing financial system.”

— H.M. Queen Máxima of the Netherlands, United Nations Secretary-General’s Special Advocate for Inclusive Finance for Development (quoted in UNEP FI, 2024)

CASE HIGHLIGHTS

- How can banks support access to affordable housing in Asia Pacific?

- How can banks leverage partnerships to boost SMEs’ access to affordable finance?

- How can banks boost financial inclusion in rural and underserved communities?

- From financial inclusion to financial health: How does UNEP FI support banks to turn ambition into action?

How can banks support access to affordable housing in Asia Pacific?

Housing affordability is a growing pressure point across the region. In Australia, for example, the National Housing Supply and Affordability Council reported in 2025 that the national median dwelling value is around eight times median household income, and that saving for a 20% deposit would take 10.6 years.[3] In New Zealand, as of 2024, median home values remain many multiples above household income, and first-home buyers still face around 10 years to save for a deposit.[4] Such dynamics directly affect household financial resilience, limiting the ability to save, invest, or withstand income shocks.

Banks can play a critical role by supporting affordable housing supply and reducing barriers to access. To quote an example, ANZ positions affordable housing as part of its broader approach to financial health and inclusion, supporting access to suitable and affordable housing through partnerships and targeted financing. The bank focuses on increasing overall housing supply, including both new social and affordable, into the market; supporting new housing models from pilot to scale, to delivery of new pipelines; and contributing funding solutions for first home buyers, specialist disability accommodation and land lease communities.

In 2025, ANZ announced financing for 156 new social and affordable homes in Southeast Queensland. The bank partnered with Queensland’s Housing Investment Fund to finance over 150 new social and affordable homes across three sites in Southeast Queensland, including Redbank, Waterford West and Miles. The project is supported by the Queensland Government’s Housing Investment Fund, which aims to accelerate the delivery of social and affordable housing through partnerships with community housing providers and private finance. It will deliver a mix of one-, two- and three-bedroom dwellings designed primarily for residents aged over 55, supporting independent living while increasing the supply of affordable housing.[5]

In New Zealand, ANZ collaborated with a Māori housing organisation to enable whānau to access homes on Māori land through a shared-equity model, combining mortgage finance with innovative tenure arrangements. These include leasehold housing on collectively owned Māori land, where the housingprovider retains a minority equity stake (e.g. 25%) and co-invests in the property, allowing families to enter with a lower initial share and progressively increase their ownership over time. This allows families who might otherwise be excluded from the housing market to secure long-term, affordable homes.[6] These approaches illustrate how banks can combine public partnerships, targeted financing, and community-based delivery models to expand access to affordable housing.

How can banks leverage partnerships to boost SMEs’ access to affordable finance?

SMEs are central to economic resilience but face persistent barriers to finance. Across emerging market and developing economies, the Micro, Small and Medium Enterprises (MSMEs) financing gap is estimated at USD 5.7 trillion, with Asia Pacific accounting for approximately 53% of the global total.[7]

In Thailand, SMEs represent over 99% of businesses and employ around 70% of the workforce.[8] As a state-owned enterprise and Thailand’s only Social Bank, Government Savings Bank (GSB) is guided by a vision to serve as a bank for social good and plays a unique role in supporting underserved groups and strengthening economic resilience through financial inclusion and social development initiatives. SMEs are one of GSB’s key focus areas, supported through a combination of government-backed lending, capacity building, and financial inclusion initiatives.

A key pillar of its approach is a government-backed soft loan program. In partnership with the Thai government, GSB provides up to THB 100 billion in ultra-low interest loans (~0.01%) to participating banks, enabling on lending to SMEs at rates not exceeding 3.5% per year.[9] As of late 2025, SMEs had drawn down nearly THB 98.7 billion from this facility, indicating strong uptake and improved access to liquidity.[10] Alongside financing, GSB also delivers large-scale financial literacy and training programs for small entrepreneurs.

These initiatives are designed with clear targets to expand access and strengthen financial capability, including structured training programs reaching approximately 50,000 small entrepreneurs annually. Together, these measures support SMEs in stabilising operations, reinvesting, and navigating economic uncertainty.

Collaboration between financial institutions, public actors and other guarantee agencies can play a major role in expanding SME financing. In South Korea, Industrial Bank of Korea (IBK) plays a leading role in SME financing, using partnerships with municipalities and credit guarantee agencies to expand access to affordable credit.

IBK partners with local government and guarantee institutions to lower financing costs through reduced guarantee fees and subsidise interest rates, particularly for SMEs facing collateral constraints. In cities such as Sejong, Goyang and Yongin, these schemes combine bank lending, municipal support and credit guarantees to reduce financing costs for SMEs. For example, in Sejong City, IBK agreed to lower guarantee fees by up to 1.2% while the city subsides interest differentials for collateral loans, making working capital financing more affordable for local firms. In Goyang City, a joint support loan programme provides up to KRW 200 billion in funds with shared guarantee and interest support, helping SMEs in manufacturing and knowledge industries access capital at lower cost. Similar partnerships with Yongin City combine bank, city and guarantee agency support to reduce loan costs and enhance liquidity for SMEs.[11]

How can banks boost financial inclusion in rural and underserved communities?

Rural and underserved communities, referring to populations with limited access to formal financial services, often face the greatest barriers, including limited physical access, lower financial capability, and higher perceived credit risk. Bridging these gaps requires delivery models that combine proximity, tailored products, and digital innovation.

In China, Agricultural Bank of China (ABC) addresses these through a combination of scale, local presence, and digital innovation. As at the end of 2025, its inclusive loan balance reached RMB 4.35trillion, while inclusive loans to small and micro enterprises amounted to RMB 3.93 trillion, serving over 5.24 million customers with outstanding loan balances. More than 40% of its domestic lending is concentrated in county and rural areas, supported by an extensive branch network and dedicated relationship managers.[12]

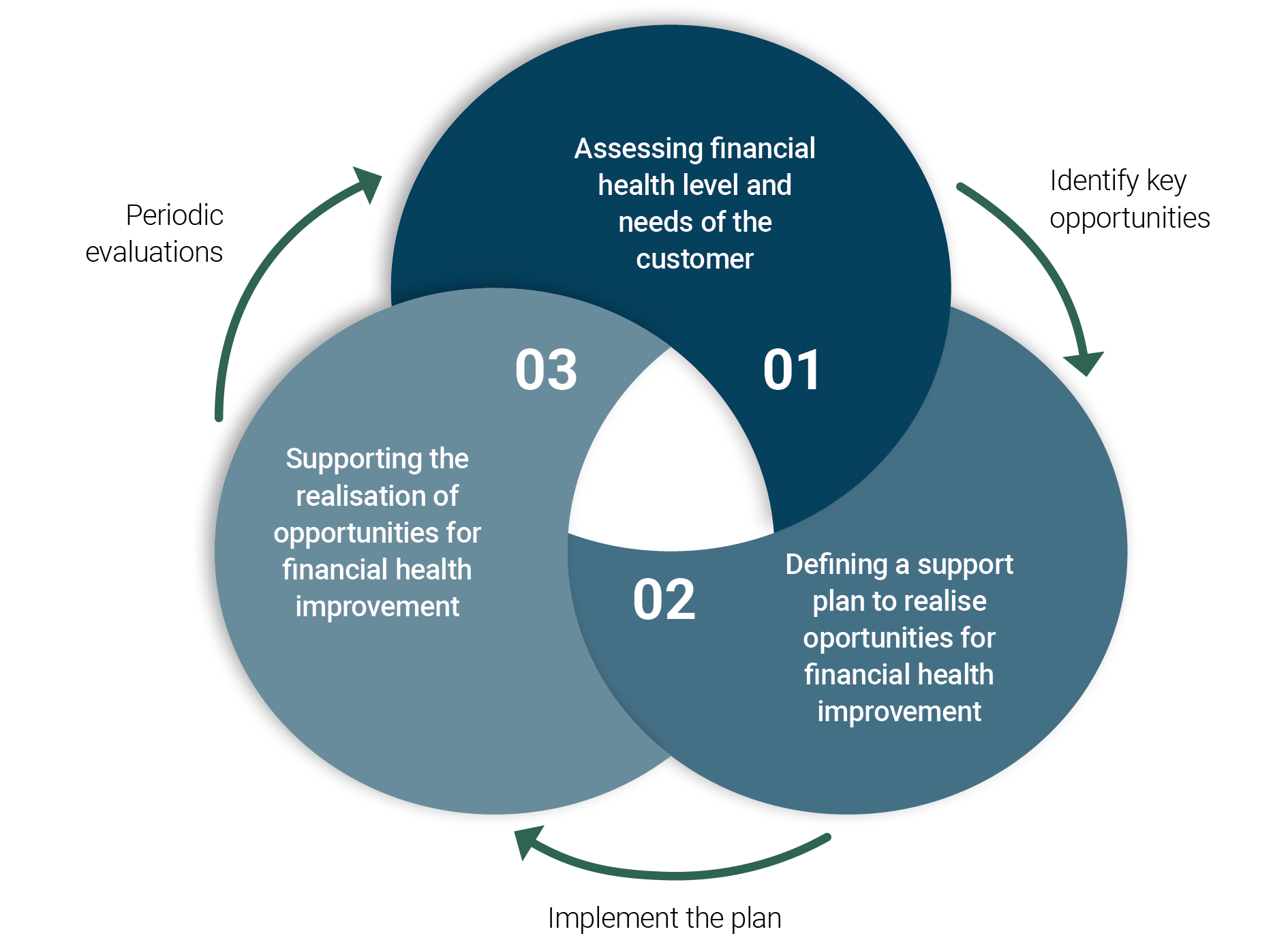

Figure 1: Approach to client engagement (UNEP FI, 2024)

ABC has developed standardised digital products such as Micro e-Loan and Huinong (agriculture and rural support) e-Loan, which reduce collateral requirements, enable online application and approvals, and automated credit assessments. With outstanding balances exceeding RMB 1 trillion, around 80% of inclusive SME lending is now delivered online.[13] Digital credit models and centralised risk management systems further support faster decision-making, improved risk control, and cost-efficient outreach. This hybrid model improves access for underserved customers while also significantly enhancing processing speed and operational efficiency, while maintaining proximity through its rural branch network.

From financial inclusion to financial health: How does UNEP FI support banks to turn ambition into action?

Expanding access is not enough. The long-term opportunity for banks lies in enabling customers to build resilience, manage risks, and improve their

financial position. This is both a social and strategic imperative. Financially healthy customers are better able to meet obligations and absorb shocks, underpinning more resilient portfolios and, ultimately, more sustainable banks. Delivering this requires embedding financial health into core business decisions, improving product design, and strengthening client engagement.

UNEP FI provides a structured approach to support this transition. Through the PRB Guidance on Financial Health and Inclusion, banks can set strategy and goals, align portfolios, and track progress, supported by practical tools and peer learning that transform ambition into effective action.[14]

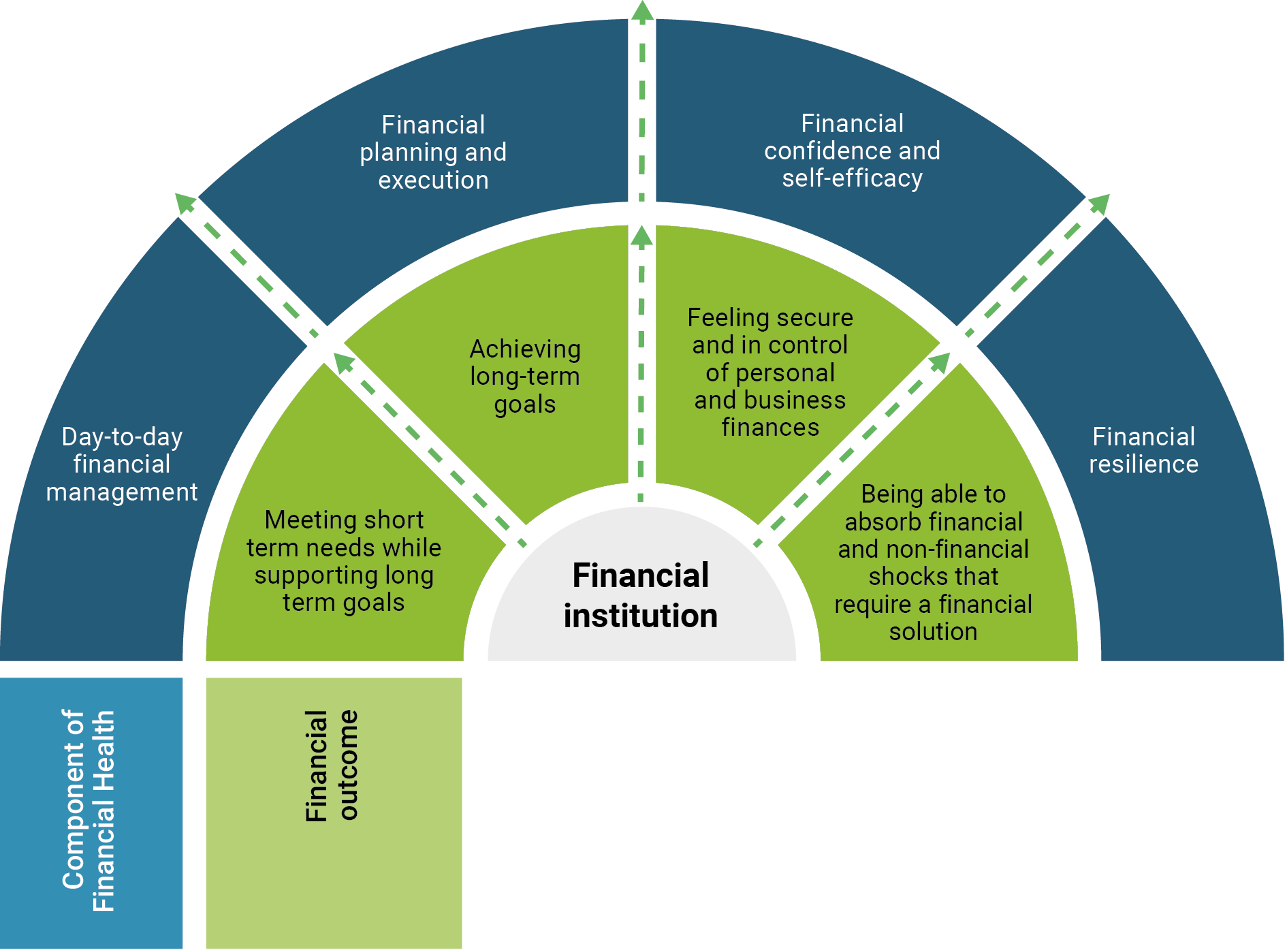

Figure 2: Financial outcomes and components of financial health (UNEP FI, 2024)

For banks in Asia Pacific, the next frontier is clear: moving beyond access to enable stronger financial health is not only a responsible banking imperative, but a business opportunity. Healthy customers are the foundation of sustainable banks. By helping customers build resilience, banks can support more stable portfolios, deepen client relationships, unlock opportunities for growth, and strengthen the long-term sustainability of the banking sector. In this sense, healthy customers are not only the foundation of sustainable banks, but part of the business case for responsible banking.

[1] World Bank (2025): Global Findex Database 2025

[2] UNEP FI (2024): Driving Impact on Financial Health and Inclusion

[3] National Housing Supply and Affordability Council (2025): State of the Housing System 2025

[4] ANZ (2024): Housing Affordability Report

[5] ANZ (2025): ANZ boosts support for social and affordable homes in Southeast Queensland with Community Housing Ltd

[6] ANZ (2025): Māori housing organisation partners with ANZ to provide affordable homes on Māori land

[7] IFC (2025): MSME Finance Gap: An updated Estimation and Evolution of the Mirco, Small and Medium Enterprises (MSME) Gap in Emerging and Developing markets

[8] The Nation (Thailand) (2026): OSMEP Launches $60 Million Relief Package to Aid Thai SMEs

[9] The Thaiger (2024): High demand for GSB soft loan scheme reaching 80 billion baht

[10] Bangkok Post (2025): Government Savings Bank rolls out fresh B100bn in soft loans for hard-hit SMEs

[11] The Asia Business Daily (2025): ‘The Go-To for SME Loans is Still Industrial Bank of Korea’… 3.6 Trillion KRW Net Increase in SME Loans from January to February

[12] Agricultural Bank of China (2025): Annual Report 2025

[13] 今日行长 (2024): 数字化浪潮席卷,农行如何打破普惠金融的“不可能三角”

[14] UNEP FI (2024): Driving Impact on Financial Health and Inclusion of Individuals and Businesses: From setting targets to implementation