Supporting clients in the transition to a nature-positive economy means embedding nature into client engagement, supporting clients through advice, financial products and solutions, and capacity building. This is both an environmental and strategic imperative. In Asia Pacific, where economies are closely tied to natural systems, enabling client transition can reduce portfolio risk, strengthen resilience, and unlock new business opportunities.

KEY TAKEAWAYS

- Nature-related risks and dependencies are becoming increasingly material across Asia Pacific

- The high dependence of economies in the region on natural systems makes transition a strategic priority

- Banks are moving from commitments to active support through sector policies, financing, and engagement

- Scaling nature-positive outcomes requires directing capital toward clients with credible nature-transition pathways and supporting their implementation

- Banks are increasingly developing financing solutions that encourage and enable nature-positive investments

Why nature matters for banks in Asia Pacific

Asia Pacific is home to some of the world’s richest ecosystems and accounts for around 20% of global biodiversity.[1] These natural systems underpin economic activity across agriculture, fisheries, forestry, tourism, water resources and other sectors that support livelihoods and economic development throughout the region. However, biodiversity loss, pollution, environmental degradation, and rapid urbanization are placing increasing pressure on these systems, with implications for long-term economic stability.

Nature loss is increasingly recognized as a business and financial issue. For banks, nature-related impacts can materialize through the impacts of nature loss on their clients, including supply chain disruption, declining productivity, resource scarcity, and physical environmental degradation. As governments, regulators, investors, and business respond to these pressures, the transition to a nature-positive economy is becoming a growing area of focus for financial institutions. This transition is also linked to evolving financing demand in areas such as sustainable agriculture, ecosystem restoration, and climate-resilient infrastructure, creating new financing opportunities.

(Click to Expand)

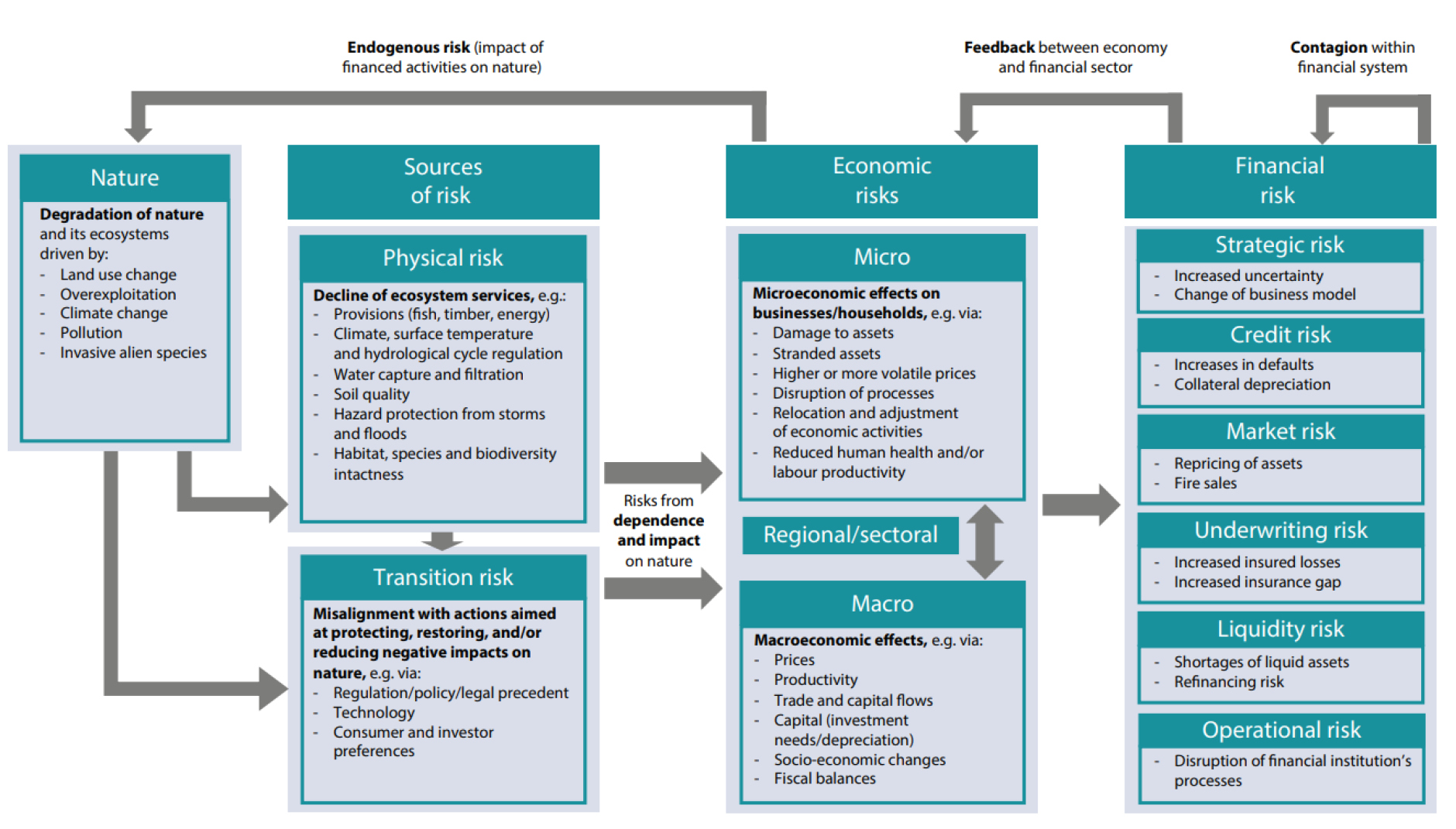

Figure 1: Overview of transmission channels in nature-based risk for FIs

Source: UNEP FI, Nature-based Risk Assessment Report (adapted from NGFS, 2023).

- +50% of global GDP is moderately or highly dependent on nature and ecosystem services

- 75% of economic activity in Asia Pacific is directly or indirectly linked to nature

- Nature-positive finance represents a USD 7 trillion transition opportunity

Source: UNEP

“The accelerating loss of biodiversity, rising water stress, soil degradation, and broader declines in natural capital pose material risks to financial institutions (FIs). As natural assets erode, the financial stability of FI clients—particularly those in nature-dependent sectors—is increasingly threatened. Managing exposure to nature-based risks is not simply reputational or regulatory, it is essential to the long-term resilience of FIs.”

— Nature-based Risk Assessment Report (UNEP FI)

CASE HIGHLIGHTS

FEATURED BANKS

How do sector policies support client transition?

CIMB (headquartered in Malaysia, with operations across ASEAN) integrates climate and nature-related considerations into its sustainable finance approach, with a focus on sectors with significant land-use impacts such as palm oil.

The bank manages deforestation and nature-related risks through its Group Sustainable Financing Policy, supported by its Sustainability Sensitive Sector list and Guidance document for high-risk commodities. In the palm oil sector, this includes the application of sustainability criteria to assess risks such as deforestation and land-use change, as well as expectations on traceability and supply chain disclosure.[2]

Since 2022, CIMB has required all palm oil clients to adopt No Deforestation, No Peat, No Exploitation (NDPE) principles as a baseline expectation for financing. Certification under national schemes such as MSPO/ISPO is required, while international standards such as RSPO are encouraged. These requirements are complemented by human rights safeguards such as free, prior and informed consent (FPIC) and grievance mechanisms. In 2025, CIMB further strengthened its approach by introducing requirements for traceability to plantation level, a defined deforestation cut-off date, and sustainability standards that apply across both client operations and third-party suppliers.[3]

Through these sector policy requirements, CIMB is integrating expectations on client practices and supporting more consistent sustainability standards across supply chains, while informing the development of financing approaches aligned with client transition pathways.

Mobilising finance for nature-positive outcomes

Across Asia Pacific, banks are increasingly developing innovative financing solutions that support nature-positive outcomes and respond to emerging environmental constraints.

Golomt Bank (headquartered in Mongolia, with a focus on domestic development and resource-linked sectors) provides an example of how nature-positive financing can be tailored to local priorities.

In 2025, the bank became the first financial institution in Mongolia to participate in a blue finance transaction through a USD160 million financing package led by IFC and supported by development finance partners.[4] Up to 15% of the facility is earmarked for blue projects that improve water efficiency, water supply, and sanitation, reflecting Mongolia’s growing need for sustainable water resource management amid increasing urbanisation and water stress. Since 2023, the Bank has secured a total of USD173 million in blue financing from impact funds and financial institutions.

Building on this, Golomt Bank has expanded its blue finance portfolio through dedicated lending for water infrastructure, sanitation and water reuse and treatment projects. Between 2024 and 2025, the Bank provided MNT 21.9 billion to support access to safe drinking water and sanitation, while introducing new lending solutions designed to increase water-use efficiency and wastewater reuse.[5]

These activities illustrate how banks can adapt to financing to address locally relevant nature-related challenges, particularly in water-stressed economies.

Embedding biodiversity into investment and financing decisions

In South Korea, SK Securities has begun incorporating biodiversity considerations into its environmental risk assessment, with integration into its ESG screening process planned. This includes identifying nature-related risks in priority sectors—industrials, energy, and real estate—where reliance on land and natural resources increases exposure to ecosystem degradation and resource constraints. The assessment combines sector-level biodiversity dependencies and impacts with portfolio exposure (AUM), helping prioritize sectors for future biodiversity strategies and supporting more informed financing decisions.

Building on these insights, SK Securities is exploring how biodiversity considerations can be reflected in its green and sustainability bond offerings and other nature-related financial products. This is intended to strengthen the company’s ability to develop financing solutions that respond to nature-related risks, while supporting clients’ transition toward more resilient business models that account for nature.[6]

Integrating nature in governance and disclosure

Mizuho Financial Group (headquartered in Japan, with a global banking and financial services footprint) demonstrates how nature considerations can be integrated into existing climate governance and disclosure processes. The bank joined the TNFD Forum in 2022 and has contributed to emerging nature-related disclosure approaches. Its analysis includes identifying sectors with significant dependencies and impacts on natural capital, including water resources and biodiversity, helping build a more structured understanding of nature-related financial risks and opportunities.

Mizuho was among the first banks in Asia to combine climate and nature related reporting into a single disclosure framework. Through its Climate & Nature-related Report, the bank aligns climate and nature considerations under a common governance, strategy, risk management, and metrics structure, reflecting the interlinkages between climate change, biodiversity loss and natural capital degradation.

By integrating nature into established climate reporting processes and applying TNFD-aligned analytical approaches across its portfolio, Mizuho provides a practical example of how financial institutions can strengthen transparency, improve risk assessment, and support clients to anticipate emerging regulatory and market expectations. [7]

Integrating nature into sustainability risk management and client engagement

Hana Financial Group (based in South Korea, with a strong corporate and retail banking presence) is strengthening its ESG risk management by integrating nature related considerations into credit assessments and client evaluations. Through ESG-based screening and risk classification processes, the bank considers environmental risks as part of lending decisions and applies enhanced review processes for sectors with higher environmental exposure. In parallel, client engagement is used to encourage better environmental management and strengthen awareness of emerging disclosure expectations. As nature-related disclosure frameworks such as TNFD gain traction, these practices also help clients prepare for more structured reporting by gradually building internal capacity for ESG data collection and transparency. Through this combination of risk integration and client engagement, Hana Bank supports the alignment of client portfolios with evolving environmental expectations and regulatory developments.[8]

From ambition to action: How does UNEP FI support banks in integrating nature into finance?

Through the responsible banking work programme, UNEP FI provides guidance, tools, and peer learning to help banks integrate nature into risk management, financing decisions, and client engagement. This includes advancing nature-related disclosure and risk assessment approaches and supporting capacity-building through partnerships with organisations such as the United Nations Sustainable Stock Exchanges Initiative, Principles for Responsible Investment, and World Business Council for Sustainable Development and the Convention on Biological Diversity (CBD).

These partnerships reflect collaboration across financial market standard setters, investor networks, and global biodiversity governance institutions. A key 2026 capacity-building initiative is the APAC Nature Reporting Preparer Forum, a regional programme bringing together 32 financial institutions across Asia Pacific to strengthen nature-related risk management and disclosure capacities.

[1] UNEP (2026): Integrating the value of nature into our economies

[2] CIMB (2026): Sustainability Report 2025

[3] CIMB (2025): Sector Guidance: Oil Palm

[4] World Bank (2026): From Scarcity to Innovation: Mongolia’s First Water Recycling System Powers Livelihoods

[5] Golomt Bank (2026): Golomt Bank recognized as “Water Ambassador” Bank for two consecutive years

[6] SK Securities (2025): SK Securities Sustainability Report 2025

[7] Mizuho Financial Group (2025): Climate and Nature-related Report 2025

[8] Hana Financial Group (2025): Hana Financial Group Sustainability Report 2024